Fees and Expenses Associated with Your Plan

Fact: Plan fiduciaries responsibility includes identifying, understanding, and evaluating fees and expenses associated with plan investments, investment options and services. Fiduciaries should also monitor any “revenue sharing” (hidden fees) made indirectly by third parties and determine if they are “fair and reasonable”. Monitoring fees and expenses is an ongoing fiduciary responsibility and an increasing level of fee litigation is currently occurring across the country.

expenses associated with plan investments, investment options and services. Fiduciaries should also monitor any “revenue sharing” (hidden fees) made indirectly by third parties and determine if they are “fair and reasonable”. Monitoring fees and expenses is an ongoing fiduciary responsibility and an increasing level of fee litigation is currently occurring across the country.

Types of "Hidden" Fees and Other Potential Fees:

- Revenue Sharing Arrangements:

- This is the practice by mutual funds or other investment providers of paying other plan service providers (i.e. third party administrator, record keeper) for performing services that the mutual fund might otherwise be required to perform.

- Bottom-line: The mutual fund has typically built into the cost of their fund charges for services they may not ultimately perform (i.e. annual expense ratio which includes the Sub-Transfer Agent Fee and 12b-1 fee) and these revenues will be shared with the actual third party service provider involved with delivery of such services.

You are required to understand any “revenue sharing” arrangements and assess the reasonableness of these fees and how they impact your plan

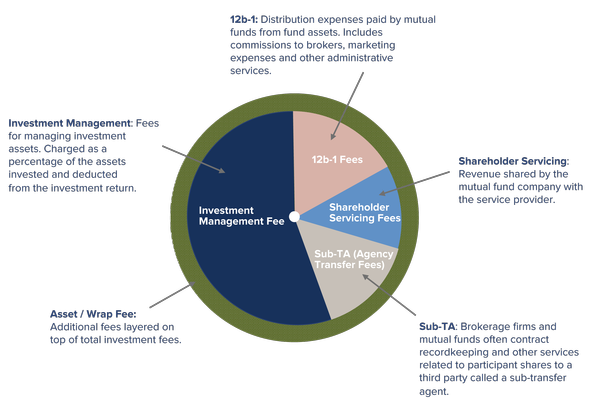

• 12b-1 Fees:

- Distribution expenses paid by mutual funds from fund assets. Generally include commissions to brokers, fees for administrative services, advertising and other marketing expenses.

- Bottom-line: Most mutual funds have varying share classes that have low to no 12b-1 fees that should be considered when applicable and a commissionable broker has an incentive to utilize funds with 12b-1 fees so as to impact their personal income as plan assets increase.

You are required to understand what 12b-1 fees are and how they impact your plan

• Sub-transfer Agent Fees:

- Fees paid to record keeper by the mutual funds available on their platform in order to reimburse for participant/sponsor level services which are provided by the record keeper.

- Bottom-line: The payment arrangement of these fees is acceptable, the issues are whether they are being disclosed (you are required to understand who is being paid what and assess the reasonableness of those fees) and whether the fees being received are “offsetting” plan costs (i.e. is the record keeper receiving Sub-transfer agent fees AND billing the plan/assets for its services, “double-dipping”).

You are required to understand what Sub-transfer Agent fees are and how they impact your plan

• Variable Annuity Wrap Fees:

- Insurance provider products which have underlying funds offered inside them. Variable annuity platforms typically not only have the expense ratio of the underlying funds to contend with but a plan level “wrap charge” to cover the structure/services provided by the insurance company. When both the expense ratio of the fund is added to the plan level charge (not always disclosed with great ease) the overall charge against plan assets is greater than the fees charged by a pure fund based platform.

- Bottom-line: The “wrap charge” associated with a variable annuity product is not unacceptable as long as when the total charge against plan assets is deemed to be “fair and reasonable” for services provided and other platforms have been considered.

You are required to understand the total plan asset charges involved in a variable annuity platform and how those charges impact your plan

• SEC Rule 28(e) Soft Dollars:

- Brokerage firms may charge extra an extra fee/commission considered to be a Rule 28(e) Soft Dollar charge. This potential extra charge can be used to purchase services (i.e. investment research).

- Bottom-line: If these fees are applicable and are deemed to be unreasonable it would be in violation of ERISA.

You are required to know whether your plan is being charged Rule 28(e) fees and if so, are these fees “fair and reasonable” for services rendered

• Investment Management Fees:

- These fees are for managing investment assets and are usually deducted directly from the investment return (as part of the annual expense ratio associated with the particular mutual fund).

- Bottom-line: The Investment Management Fee can vary greatly from fund to fund and since it has a direct relationship to the net return should be benchmarked against other funds with similar objectives.

You are required to demonstrate a process of benchmarking fees and expenses which impact your plan

Variable annuities are long-term investments designed for retirement purposes. Variable annuities are subject to insurance related charges including mortality and expense charges, administrative fees, and the expenses associated with the underlying funds. Early withdrawals are subject to company-imposed surrender charges. Withdrawals are also subject to ordinary income tax, and if taken prior to age 59½, a 10% federal tax penalty may apply. Investment involves risk, including the possible loss of principal. Your contract value when redeemed may be worth more or less than your original investment.

Mutual funds and variable annuities are sold by prospectus only. Before investing, investors should carefully consider the investment objectives, risks, charges and expenses of a mutual fund, or a variable annuity and its underlying investment options. For mutual funds, the fund prospectus, and for variable annuities, the current contract prospectus and underlying fund prospectuses, provide this and other important information. Please contact your representative or the Company to obtain a prospectus. Please read the prospectus(es) carefully before investing or sending money.