Responsibilities Under ERISA §404(a) and §404(c)

Overview of ERISA §404(a) and §404(c)

When was the last time you reviewed your basic fiduciary responsibilities?

At your next Investment Committee meeting, consider a discussion around the basic guidelines as set forth by ERISA Section 404(a) and Section 404(c). If you do not have an Investment Committee that currently holds fiduciary responsibility for your retirement plan, please contact 401(k) & 403(b) Fiduciary Advisors for best practices in forming one.

The core fiduciary responsibility under Section 404(a) is to maintain and follow a written plan document that complies with ERISA and when making decisions that affect the plan, ensure that these decisions are made prudently and “solely” on behalf of and for the exclusive benefit of the plan participants and their beneficiaries.

Even when participants have full control of investment decisions, plan fiduciaries could still be responsible for participant investment choices. Fortunately, plan fiduciaries do have an option that offers certain protections. An effective method of managing this risk rests in Section 404(c) of the Employee Retirement Income Security Act of 1974, as amended (ERISA). This provision generally allows fiduciaries to be relieved of liability for participants' investment decisions.

While not all-encompassing, the following acts as a primer in regards to ERISA §404(a) and §404(c).

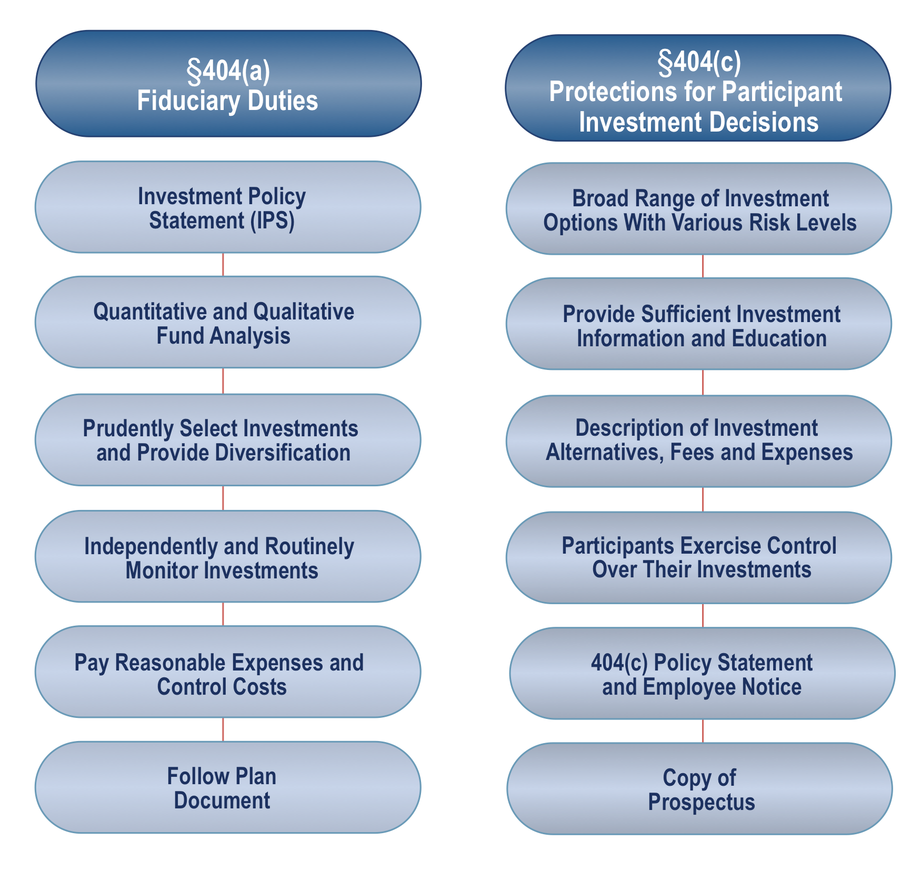

ERISA §404(a)

ERISA §404(a) collectively represents the fiduciaries’ duties and responsibilities in regards to selecting, monitoring and replacing (when needed) the plan’s investment options. Basic compliance items would include:

- Maintenance of an Investment Policy Statement (IPS), which is designed to provide a process by which the investment options are measured and monitored

- Utilizing quantitative and qualitative analytics to independently and routinely monitor the investment options; the ScorecardSM System that is utilized by 401(k) & 403(b) Fiduciary Advisors. was designed as an effective tool to document this requirement

- Prudently select investments with care and in a judicious manner that provides diversification

- Periodic review of investment recommendations and policies, which are part of each quarterly fiduciary investment review, provided by your plan’s consultant

- Documentation of the Investment Committee meeting process and documentation of annual plan review meetings

- Paying reasonable expenses and controlling plan

ERISA §404(c)

Does your plan intend to comply with §404(c)? ERISA §404(c) relieves plan sponsors and other fiduciaries from liability for losses resulting from participants’ direction of their investments. This protection applies only to participant-directed investments, and not to investments required under the plan or directed by the plan sponsor, such as employer stock. To take advantage of ERISA §404(c), the plan must satisfy three categories of requirements:

- Investment menu requirements

- Plan design and administrative requirements

- Information and disclosure requirements

To provide fiduciaries the protection from potential losses that result from participant-level investment decisions, ERISA §404(c) outlines certain requirements. High level, but not comprehensive, compliance items would include:

- Offering a broad range of investment alternatives with various risk level characteristics

- Providing a description of the investment options with the fees and associated plan expenses

- Allowing participants to give instructions on how to invest their account and provide participants with the ability to transfer among investment options; it is important that participants have ultimate control of where they invest their money

- Providing participants with sufficient information and education about the plan and its operations to make informed decisions

- Allowing participants to exercise independent control over their investments

- Ensuring the plan’s default fund meets the requirements of the qualified default account (QDIA) rule

A final key element to §404(c) is to periodically notify participants of your intention to comply with this requirement. The most effective way to do so is through the periodic distribution of a §404(c) Notice and Policy Statement.